What Does the Q Ratio Say About the Market’s Valuation?

In the last few issues of this Commentary, we have discussed various measures for valuing the stock market. As I have noted, some of the measures we have been using to value the market are identical to, or similar, to ratios and valuation metrics that we use to value individual securities. One of these ratios is the price-to-earnings ratio which we use on a regular basis and post weekly in the Stock Market Valuations section of this weekly Commentary. The price-to-earnings ratio we use to value the market is identical to the price-to-earnings ratio we use to value individual securities. Another ratio we use to value the market, which we discussed last week, is the Buffett Indicator . As noted in the article on the Buffett Indicator, it is very similar to a price-to-sales ratio used to value individual stocks.

This week we will discuss Tobin’s q ratio, which is similar to a price-to-book ratio used to value individual securities. Tobin’s q is the ratio between a physical asset’s market value and its replacement value. It was developed by economist Nicholas Kaldor in 1966, but later popularized by Nobel Laureate economist James Tobin. Tobin describes the composition and adaptation of the q ratio for the markets and the economy this way (Tobin & Brainard, 1976): “One, the numerator, is the market valuation: the going price in the market for exchanging existing assets. The other, the denominator, is the replacement or reproduction cost: the price in the market for newly produced commodities. We believe that this ratio has considerable macroeconomic significance and usefulness, as the nexus between financial markets and markets for goods and services” (pp. 1-2).

One popular use for the q ratio is to determine the valuation of the whole market in relation to aggregate corporate assets. The formula for this is: q = value of the stock market / corporate net worth. Tobin hypothesized that the combined market value of all the companies in the stock market should be approximately equal to their replacement costs. A ratio greater than one would indicate that the market is overvalued. A ratio less than one would imply that the market is undervalued.

The fair-market valuation of 1:1 does not always hold though. According to Hayes (2019), “…the average (arithmetic mean) Q Ratio is about 0.70. This number, however, fluctuates: The all-time Q Ratio high at the peak of the 2001 Tech Bubble was 1.61, which suggests that the market price was 136% above the historic average of replacement cost at the time. The all-time lows occurred in 1921, 1932 and 1982 when they stood around 0.30, which is approximately 55% below the replacement cost.” Mislinski (2020) has more updated statistics that support these general valuation conclusions.

What does Tobin’s Q tell us about the current market valuation? The graph under Charts for Review and Thought (below) is an example of Tobin’s q for all U.S. corporations. The line shows the ratio of the US stock market value to U.S. net assets at replacement cost since 1900. The current q ratio would plot well above the average on this chart. Advisor Perspectives shows current data on the market’s valuation using the q ratio. Advisor Perspectives’ Mislinski (2020) estimates that the latest datapoint for the q ratio is currently 151% above the mean. These indicators using the q ratio all point to substantial market overvaluation.

As we discussed last week in our discussion of the Buffett Indicator, do these measures of overvaluation mean that the market is poised for an imminent crash? While the sky-high valuations tell us that the market could, and probably should decline, based on our expectations of the future economic climate; markets can and do stay overvalued for very long periods of time. As discussed in a previous Commentary, Is the Stock Market A System 1 Thinker?, I noted that, “The calculation of the Intrinsic Value Line reflects System 2 thinking, whereas the daily market fluctuations around that line reflect System 1 thinking.” What this means is that the market currently is functioning in the System 1, highly emotional realm. How long it stays in that realm cannot be predicted with any degree of certainty. I can only tell you that the market is very overvalued based on our research into a number of stock market valuation indicators, including the Buffett Indicator. But as Jesse Livermore, who was a famous and successful stock market investor in the early part of the last century said: “The market does what it should do, but not always when.”

References

Hayes, A. (2019, June 24 2019). “What is Q Ratio – Tobin’s Q.” Retrieved September 8, 2020, from https://www.investopedia.com/terms/q/qratio.asp#:~:text=The%20Tobin’s%20Q%20ratio%20equals,market%20value%20equals%20replacement%20cost.&text=While%20Tobin%20is%20often%20attributed,economist%20Nicholas%20Kaldor%20in%201966.

Mislinski, J. (2020). “The Q Ratio and market valuation: August update.” Retrieved September 2 2020, from https://www.advisorperspectives.com/dshort/updates/2020/09/02/the-q-ratio-and-market-valuation-august-update.

Smithers, A. and S. Wright (2000). Valuing Wall Street: Protecting wealth in turbulent markets. New York, Mc-Graw Hill.

Tobin, J. and W. C. Brainard (1976). Asset markets and the cost of capital. Y. University. Yale University.

Reference

Buffett, W. and C. Loomis (2001). Warren Buffett on the stock market. Fortune. New York, Fortune Media Group Holdings. December 10, 2001

Economic and Investment Highlights

Last Week

Coronavirus cases surpassed 25 million globally.

Banks are bracing for a wave of defaults and expect a longer, deeper recession than they had expected in the Spring.

India’s GDP fell 23.9% last quarter.

Fuel consumption by U.S. drivers is slowing.

U.S. factory output grew in August, but employment was mixed. The unemployment rate fell to 8.4% in August from 10.2% in July. Unemployment was close to 15% in April and 3.5% in February.

U.S. debt climbed to its highest level compared to gross domestic product (GDP) since World War II and is projected to exceed GDP next year.

The Dow rose above 29000 for the first time since February.

United plans to cut 16,370 staff.

Australia fell into a recession for the first time in 29 years. Its GDP fell 7% in the second quarter.

Chicago Fed Chief Evans said the U.S. economy needs continued support from the government.

The Dow, the S&P 500 and the Nasdaq fell for the week. The Dow was down 1.8%; the S&P 500 was down 2.3%; and the Nasdaq was down 3.3%. The 10-year treasury yield ended the week at 0.720%. Gold closed at $1,923.90 for the week. Oil closed at $39.77 for the week.

The Week Ahead

This link takes you to Econoday’s Economic Calendar and Economic Events and Analysis which shows the upcoming economic reporting events scheduled in the week and months ahead.

Summary

Note: The models below may not capture the impact of COVID-19 beyond their impact on GDP source data and relevant economic reports that have already been released. They may not anticipate the impact of COVID-19 on forthcoming economic reports beyond the standard internal dynamics of the models.

Note: The comments that follow are derived from the economic indicators referenced in the Resources section of this newsletter and other sources in this report.

The Aruoba-Diebold-Scotti Business Conditions Index (ALS) had been trending up for several weeks from having dipped in 2019. Recently with the advent of the economic collapse, the index crashed. It has now been generally trending down again, but fluctuating within a narrow band. This is a slightly positive indicator for the economy on a short-term basis.

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the third quarter of 2020 is 29.6 percent. This reading agrees with the ALS model assessment of an improving short-term economic environment.

The New York Fed Staff Nowcast stands at 15.68 percent for 2020:Q3 and 7.27 percent for 2020:Q4.

The Chicago Fed National Activity Index (CFNAI) showed an increase in economic activity in June. The Chicago Fed National Activity Index (CFNAI) was +1.18 in July, down from +5.33 in June.

All told, these short-term economic indicators are a mixed analysis for the economy, at least on a short-term basis.

Expectations that stock prices will rise over the next six months is now at 23.7% in a recent AAII Sentiment Survey. The historical average is 38.0% for the survey. 27.8% of the investors in the survey described their short-term outlook as neutral and 48.5% were bearish. Please see the AAII Sentiment Survey for the complete results.

The latest Gross Output (GO) reading (July 6, 2020) showed that Gross Output slowed significantly in the first quarter of 2020.

On a longer-term basis, the forecasters in the Philadelphia Fed’s Survey of Professional Forecasters (as of August 14, 2020) predict real GDP will increase at 19.1 percent for the third quarter of 2020, 5.8 percent in the fourth quarter of 2020, 5.2 percent in the first quarter of 2021, 3.8 percent in the second quarter of 2021, and 3.6 percent in the third quarter of 2021. On an annual-average over annual-average basis, the forecasters predict real GDP to contract -5.2 percent in 2020; and grow 3.2 percent in 2021, 3.5 percent in 2022 and 2.2 percent in 2023. The forecasters predict the unemployment rate will be 10.0 percent in Q3 and 9.5 percent in Q4; and will be 9.0 percent in 2020; 8.0 percent in 2021, 6.0 percent in 2022, and 5.3 percent in 2023. The next survey release date is November 16, 2020.

The National Association for Business Economics (NABE) released an Outlook Flash Survey on April 10, 2020. The NABE panel expects GDP declines in Q1 2020 and Q2 2020, and upticks in Q3 2020 and Q4 2020. The panel believes the U.S. economy is already in a recession and predicts real GDP will grow at an annual rate of -2.4 percent for the first quarter of 2020, -26.5 percent for the second quarter of 2020, 2.0 percent in the third quarter of 2020, 5.8 percent in the fourth quarter of 2020, and 6.0 percent in the first quarter of 2021. The forecasters expect unemployment to average 3.8% in Q1 2020. The median unemployment rate projection for Q2 2020 is 12.0%. The unemployment rate is expected to fall back to 9.5% at the end of 2020, and to 6.0% at year-end 2021. The panel’s forecast for the PCE price index less food and energy calls for a slowdown in the annual rate of change from 1.7% in Q1 to 0.8% in Q2 2020. The panel expects the rate to increase gradually to 1.7% in the last half of 2021.

For a more in-depth review and analysis of the economy, please see our mini-book on economic analysis and forecasting entitled: Simple and Effective Economic Forecasting.

Stock Market Valuations

Our estimates of the market valuations for two stock market indices, the Dow Jones Industrial Average (DJIA) and the Standard & Poor’s 500 (S&P 500), can be found in the file below:

Conclusion

During this time of global flux due to the coronavirus, I am leaving the Conclusion discussion below the same as was posted on March 23, 2020. The March 23, 2020 discussion still adequately reflects my thinking on the current state of affairs.

Important Note: While I don’t believe it is time to jump back into the stock market in a big way because of the market’s overvaluation, I have been advising the last few of weeks in this Commentary and in my weekly podcast, Intrinsic Value Wealth Report Radio, that investors can continue building their investment portfolios by selecting individual securities that offer growth and value opportunities.

Reprinted from March 23, 2020

Up until the past week, the economy had been in a stable but somewhat vulnerable state. Nonetheless, it had remained fairly strong. In fact, robust consumer spending and strong labor market conditions had given us confidence that the economy, which had been in its tenth year of expansion, could continue to grow. But we were cautious on this outlook. There were several reasons for our caution. U.S. business growth had been mixed. And global economic growth had been mixed as well. The new coronavirus was becoming a global economic threat, although it was still too early to tell how much of an effect it would ultimately have. Debt is at high levels for consumers, businesses, and government (at all levels of government). Finally, this is an election year that will likely have significant consequences either positively or negatively depending on the outcome of the elections. And of course, it is still too early to tell what the outcome of the elections will be.

In just a few days, the coronavirus’s effect on the economy and the markets went from a ripple to a tsunami. Businesses are shuttering, events are being cancelled or postponed, grocery store shelves are empty, and people are being asked or ordered to stay home. The markets are now deep in bear market territory. The effects on the economy, even given the short time that the economy has been retreating, may be with us for a long time. There is now a much greater risk of a recession, and there has even been some talk of a depression. The government, the Fed, Republicans, and Democrats, and pretty much the entire country, is trying to get the virus under control and is coming up with plans to mitigate the long-term economic effects caused by the virus. But the virus has impacted the economy – in a significant way – in just a short time. How long lasting the effects will be no one can tell right now. The economy has been largely shut down and remains so today. It takes time to restart the economy after a situation such as what is occurring at the present time.

Given these events and the rapidly deteriorating situation, as I said last week, I would caution not to panic. The economy and the markets will get better. The situation is bad – there is no doubt about that – but it will turn around. The real question is when will it turn around? No one knows that at the present time. But it will turn around.

For now, review your investment portfolios. It is highly likely that all or most of your stocks are down. You should not consider selling the bulk of your stocks – only consider selling companies that are not sound companies. But do recognize that as the economy deteriorates, even good companies will be affected.

For stock market value hunters, we believe it is still too early to jump back in. We will be closely monitoring the markets using the many tools and models that we have developed over the years to assess the economy and the markets. We will use our best judgement and thoughts to let you know when we believe things are turning around. The turnaround hasn’t happened yet.

We believe it is important to maintain a long-term view toward investing. But for now, just sit tight. Eventually, this means that you should continue building your investment portfolio using the Cassandra Stock Selection Model to select individual securities that offer growth and value opportunities.

Chart for Review and Thought

Source of data: Valuing Wall Street (http://valuingwallstreet.com/index.shtml). The data from 1952 on comes from the “Flow of Funds Accounts of the United States Z1”, which is published quarterly by the Federal Reserve. Earlier data are available from a variety of sources from 1900 as compiled by Stephen Wright, University of London. Wikipedia https://en.wikipedia.org/w/index.php?title=Tobin%27s_q&oldid=972541110

Simple and Effective Economic Forecasting Model

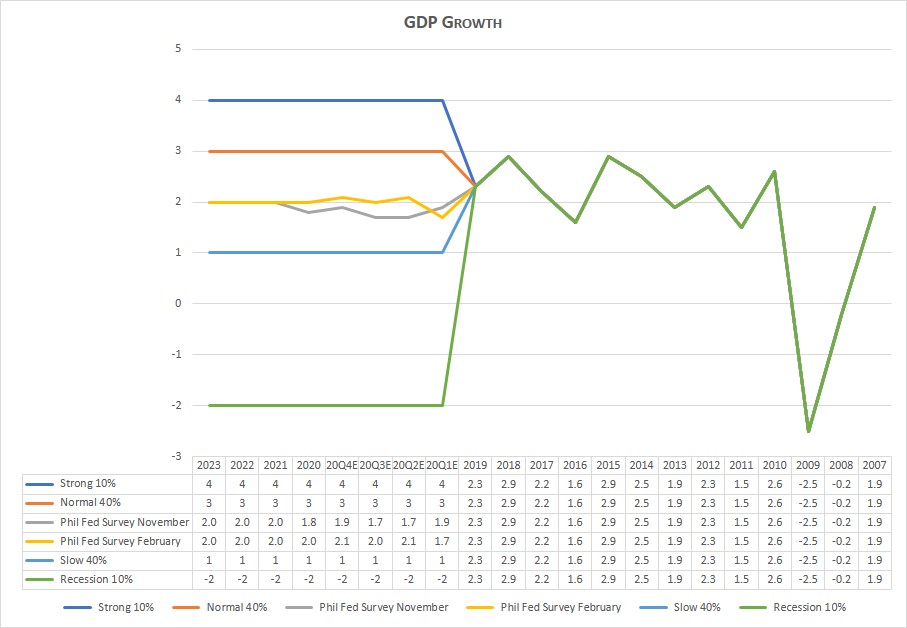

Note: The table and chart below have not been updated. However, we believe that a recession is quite likely. In the chart below, the bottom green line shows what a recession could look like.

Notes (GDP Growth Chart):

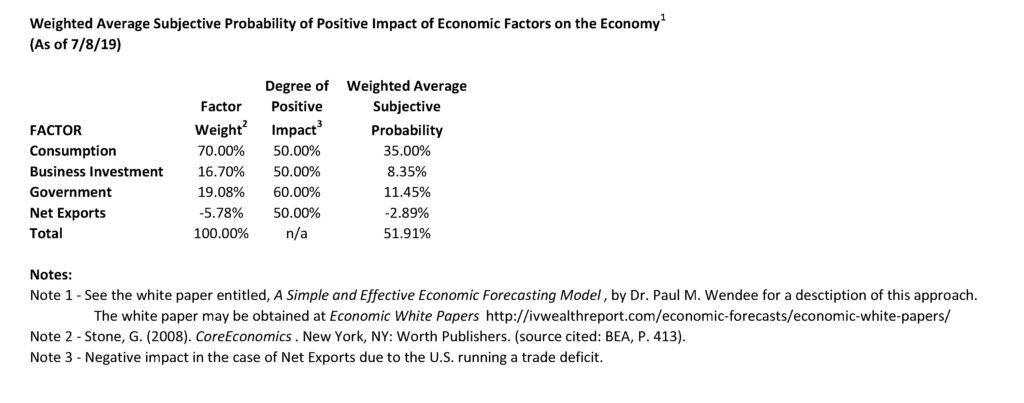

- See the July 8, 2019 Commentary for an introduction to this model.

- Actual numbers 2007 through 2019; forecasted numbers thereafter.

- Normal GDP growth is typically in the 2% to 3% range.

- A recession is generally defined as two consecutive quarters of negative economic growth as measured by a country’s gross domestic product (GDP).

Thought for the Week

Yogi Berra once went to a restaurant and ordered a whole pizza. “How many slices should I cut,” asked the waitress, “four or eight?” “Better make it four,” said Yogi. “I’m not hungry enough to eat eight.”

Announcements

The Intrinsic Value Wealth Report has started a new YouTube channel called Intrinsic Value Wealth Report TV. You can view the YouTube channel at Intrinsic Value Wealth Report TV.

The Intrinsic Value Wealth Report has started a new podcast called Intrinsic Value Wealth Report Radio. You can listen to the podcast at Intrinsic Value Wealth Report Radio.

Dr. Wendee spoke at the Investment Club of America’s annual economic summit, called Econosummit, on Sunday March 1, 2020 in Las Vegas.

Dr. Wendee attended the The National Due Diligence Alliance (TNDDA) investment banking conference, which was held March 6-8, 2020 at the Four Seasons Resort in Dallas, Texas. This is a conference held several times throughout the year for investment bankers and registered investment advisers to learn about new opportunities in the Alternative Investment asset classes.

We have been researching the use of crowdsourcing for investment ideas. We will be sending a survey out in the next few weeks to get your input on the economy and the markets; and to get any investment ideas that you would like to share. We will compile this input and distribute the results to you and our other subscribers. We have been testing our crowdsourcing models with students and have been having good success and results.

Dr. Wendee has been researching and writing a new theory of economics known as, The Value Creation Theory of the Economy (also known as, Intrinsinomics). The full paper on Intrinsinomics will be published in the near future.

Finance 3350: Personal Finance-Portfolio & Risk Management– Dr. Wendee started teaching Finance 3350 – Portfolio & Risk Management at California State University, Los Angeles (CSULA) for the Summer term starting May 2020. Dr. Wendee teaches courses in Management and Finance at CSULA.

Business 548: Strategy and Decision Making – Dr. Wendee will be teaching Business 548 – Strategy and Decision Making at California Baptist University (CBU) starting at the end of June 2020. Dr. Wendee teaches courses in Finance, Business, Strategy & Decision Making, and Economics at CBU.

Business 303: Business Finance – Dr. Wendee will be teaching Business 303 – Business Finance at California Baptist University (CBU) starting at the end of August 2020. Dr. Wendee teaches courses in Finance, Business, Strategy & Decision Making, and Economics at CBU.

Dr. Wendee presented a paper on his new theory of economics known as, The Value Creation Theory of the Economy (also known as, Intrinsinomics), at the International Leadership Association’s annual global conference which was held in Ottawa, Canada last Fall.

Dr. Wendee will present an updated paper on his new theory of economics known as, The Value Creation Theory of the Economy (also known as, Intrinsinomics), at the International Leadership Association’s annual global conference which will be held in San Francisco, California in November.

Dr. Wendee is working on a financial planning modeling program which will be available in the near future. The modeling program is designed to assist anyone in creating a financial plan and is customizable for each person’s unique financial planning goals. A working draft of the model is currently in beta test with students. Click this link, schematic, to go to the clickable document under the subheading Financial Planning Process (Draft) in the Intrinsic Value Wealth Report to see a draft of the schematic for the new financial planning process.

Dr. Wendee has been developing an econometric model specifically designed to monitor and forecast the global economy as this current economic crisis unfolds. This new econometric model is based on other econometric models that he has designed and have used for many years. You can find some of these earlier models in Book # 6 – Simple and Effective Economic Forecasting in the sister website to this website which is called the Intrinsic Value Wealth Report. The new econometric model has been constructed with some additional tools and methods that he has learned and some that he has developed over the last several years. He will be talking more about this new econometric model in this Commentary over the next few months. His comments and forecasts on the economy and the markets going forward will be based to a significant extent on this new model.

We have begun raising capital for our fund-of-funds investment, Northwest Quadrant Opportunity Fund, LLC. The fund engineers and constructs an investment vehicle consisting of Alternative Asset investments. The fund’s objective is to build a diversified portfolio of strong, solid, steady- performing assets, with highly qualified asset managers who have proven track records that meet our underwriting requirements. To learn more about the Northwest Quadrant Opportunity Fund, LLC and to obtain an offering memorandum, please click Northwest Quadrant Opportunity Fund, LLC.

Intrinsic Value Wealth Creation pyramid

We always conclude our commentary with a discussion of the Intrinsic Value Wealth Creation Pyramid. The Intrinsic Value Wealth Creation Pyramid is designed to show some of the major categories for building wealth. It is the result of many years of study of the wealth building process; experience working with clients who have built considerable wealth; and my own personal experience building wealth. Newsletter subscribers should consult the Intrinsic Value Wealth Creation Pyramid as one of many useful investment tools while considering their investment plans.

The chart in this section is an expanded version of the Intrinsic Value Wealth Creation Pyramid Chart referenced in the Forbes.com article entitled, Nine Of The Best Ways To Build Wealth.

RESOURCES

See our Resources section for links to economic and other resources used in the preparation of this Commentary.