No Surprise That Berkshire Underperformed the S&P 500 Over The Past Decade

It came as no surprise to me to learn this past week that Warren Buffett’s Berkshire Hathaway had underperformed the S&P 500 in the last decade. Berkshire Hathaway stock was up 259% in the past decade versus the S&P 500’s return of 314% in the same period. The overall return comparison since 1965 looks much better. Berkshire Hathaway has produced a 21% annual compounded return from 1965 to the end of 2018 versus 9.7% for the S&P 500 including dividends. It is this latter return comparison that has made Warren Buffett revered as a stock investing legend. And to be clear, I am an ardent follower of Warren Buffett and his stock picking prowess as well.

Warren Buffett uses a value stock picking strategy whereby he tries to find stocks that are undervalued relative to their “intrinsic value” (for more on intrinsic value, see my Book #2 – Think Strategically, Think Value). Many analysts contend that Berkshire has become too large, and is holding too much cash, to be able to find truly undervalued deals; and that this has hampered its ability to find the very undervalued opportunities that have helped Berkshire’s performance in the past.

In fact, much of Berkshire’s stellar early performance came from buying entire companies and growing them; and from buying stocks in the stock market that were very undervalued. This is more difficult to do as the large conglomerate that Berkshire has become. Berkshire currently has a stock market value of around $537 billion. Furthermore, because of the difficulty of finding investments that suit its value orientation, Berkshire is sitting on well over $100 billion in cash.

I would also contend that with a portfolio of around 60 stocks, Berkshire has become somewhat of a closet indexer. Good diversification can often be achieved with around 25 to 30 stocks. At 60 holdings, Berkshire’s returns over time are likely to approximate the returns of the overall market. That is the penalty for becoming too big! Although, it could be argued that becoming too big is a nice problem to have.

Economic and Investment Highlights

Last Week

Uber’s stock price slid 7.6% below its IPO price of $45, which was already a conservative pricing of the stock for its stock’s public debut. Uber’s IPO was conducted on Friday. The stock price decline still left Uber with an approximately $76 billion market valuation, making it one of the most valuable U.S. startups.

The U.S. imposed tariffs of 25% on $200 billion of Chinese goods and U.S. China trade talks ended with no agreement. This raises the fear of diminishing economic activity if the U.S. and China remain at odds. However, both the U.S. and China gave strong indications that the trade negotiations are not yet over and expressed some optimism for future talks.

The Fed said that the increase in risky corporate debt is a major vulnerability of the U.S. financial system. We have been citing this concern for quite some time (see for example our Economic and Investment Review in the Winter edition of this newsletter).

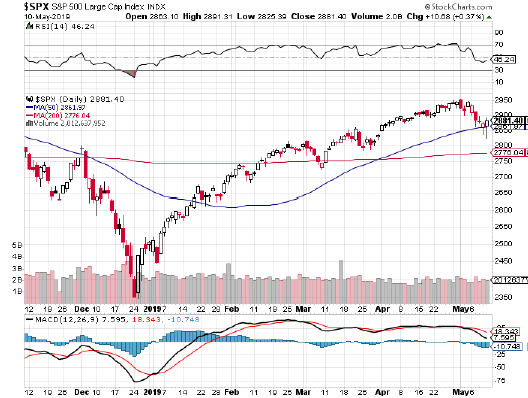

The stock market declined last week posting its largest weekly drop for 2019. Please see the S&P 500 chart below.

Occidental Petroleum agreed to a $38 billion purchase of Anadarko Petroleum.

In a Wall Street Journal poll of economists, the majority of the economists polled expect strong wage growth in the coming year due to a continuing tight labor market.

The Week Ahead

This link takes you to Econoday’s Economic Calendar and Economic Events and Analysis which shows the upcoming economic reporting events scheduled in the week and months ahead.

Summary

Note: The comments that follow are derived from the economic indicators referenced in the Resources section and other sources at the end of this report.

The Aruoba-Diebold-Scotti Business Conditions Index (ALS) has been trending up the last several weeks and is now very close to the zero line. The ALS Index advanced slightly again this past week. This is a very positive indicator for the economy on a short-term basis.

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the second quarter of 2019 is 1.6 percent on May 9, down from 1.7 percent on May 3. This slight adjustment continues to support the ALS model assessment of an improving short-term economic environment.

The New York Fed Staff Nowcast stands at 2.2% for 2019:Q2.

The Chicago Fed National Activity Index (CFNAI) showed a slight pickup in economic activity in March. The index was –0.15 in March, up from –0.31 in February.

All told, these short-term economic indicators are a positive analysis for the economy, at least on a short-term basis.

Expectations that stock prices will rise over the next six months increased another 4.1 percentage points to 43.1% in the latest AAII Sentiment Survey. The rise puts optimism a little over the historical average of 38.5% for the survey. Please see the AAII Sentiment Survey for the complete results.

The latest Gross output (GO) reading suggests slow economic growth as we enter 2019.

On a longer-term basis, the forecasters in the Philadelphia Fed’s Survey of Professional Forecasters (as of March 22, 2019) predict real GDP will grow at an annual rate of 1.5 percent this quarter and 2.4 percent next quarter. On an annual-average over annual-average basis, the forecasters predict real GDP to grow 2.4 percent in 2019, 2.0 percent in 2020, and 1.8 percent in 2021. The forecasters predict the unemployment rate will average 3.7 percent in 2019 and 2020, 4.0 percent in 2021, and 4.2 percent in 2022.

For a more in-depth review and analysis of the economy, please see our mini-book on economic analysis and forecasting entitled: Simple and Effective Economic Forecasting.

Stock Market Valuations

Our estimates of the market valuations for two stock market indices, the Dow Jones Industrial Average (DJIA) and the Standard & Poor’s 500 (S&P 500), can be found in the file below:

Conclusion

We continue believe the economy is in a stable but somewhat vulnerable state. Nonetheless, it has remained fairly strong. In fact, the extremely strong first quarter GDP showing and the strong labor market conditions give us more confidence that the economy, now in its tenth year of expansion, can continue to grow. Please see our complete Economic and Investment Review in the Winter 2019 quarterly issue of the Intrinsic Value Wealth Report Newsletter.

Even with the pullback in the market this past week, it remains overvalued. But that does not mean that a market correction is imminent. Markets can and do stay overvalued for long periods of time. As discussed above in the Economic and Investment Highlights section of this Commentary, we believe the economy is in a stable but vulnerable state. If the economy remains strong, the markets will likely remain strong. If the economy deteriorates, the markets may well correct. There are other events that could trigger a market correction, of course, but economic conditions are the most likely and foreseeable events that could make that happen.

We believe it is important to maintain a long-term view toward investing. This means that you should continue building your investment portfolio using the Cassandra Stock Selection Model to select individual securities that offer growth and value opportunities.

Chart for Review and Thought

S & P 500 – The S & P 500 posted its largest weekly drop for 2019 last week.

Announcements

We have been researching the use of crowdsourcing for investment ideas. We will be sending a survey out in the next few weeks to get your input on the economy and the markets; and to get any investment ideas that you would like to share. We will compile this input and distribute the results to you and our other subscribers.

Dr. Wendee will be speaking at the Las Vegas Investment Club on June 24th. He will be speaking on the topic of his popular Forbes article, Nine of the Best Ways to Build Wealth. Please contact Mike Lathigee at mike@mikelathigee.com if you would like to attend.

Dr. Wendee will be speaking at FreedomFest during its annual conference in Las Vegas, July 17 – 20, 2019.

Dr. Wendee will be a judge at the FundingPost June PitchFest Event on June 11, 2019 in San Diego. Click on this link for details on the event:

https://www.fundingpost.com/event/reg1.asp?event=433

Dr. Wendee attended and did coursework at the International Business Brokers Association (IBBA) meeting in Orlando this past weekend. He will be attending the Money show in Las Vegas this coming week.

IBBA Conference

May 10 – 12, 2019

Intrinsic Value Wealth Creation pyramid

We always conclude our commentary with a discussion of the Intrinsic Value Wealth Creation Pyramid. The Intrinsic Value Wealth Creation Pyramid is designed to show some of the major categories for building wealth. It is the result of many years of study of the wealth building process; experience working with clients who have built considerable wealth; and my own personal experience building wealth. Newsletter subscribers should consult the Intrinsic Value Wealth Creation Pyramid as one of many useful investment tools while considering their investment plans.

The chart in this section is an expanded version of the Intrinsic Value Wealth Creation Pyramid Chart referenced in the Forbes.com article entitled, Nine Of The Best Ways To Build Wealth.Intrinsic Value Wealth Creation PyramidDownload

RESOURCES

Economic Indicators

Below are links to a few of the many resources that we follow on a continuous basis to track the economy and financial markets on a short-term and long-term basis.

Real-Time and Current Economic Conditions

The Federal Reserve Bank of Philadelphia’s Aruoba-Diebold-Scotti Business Conditions (ADS) Index is designed to track real business conditions at high frequency. Click Aruoba-Diebold-Scotti Business Conditions Index to access this model.

Click GDPNow to access The Federal Reserve Bank of Atlanta’s GDPNow Forecasting Model.

The Federal Reserve Bank of New York’s Nowcast report tracks the evolution of the FRBNY Staff Nowcast of GDP growth and the impact of new data releases on the forecast. Click Nowcast to access the report and background information on the report.

The Chicago Fed National Activity Index (CFNAI) is a monthly index designed to gauge overall economic activity and related inflationary pressure. Click CFNAI to access this index.

Economy At A Glance

The National Economic Trends charts provided by the Federal Reserve Bank of St. Louis (FRED) can be accessed by clicking the Economy At A Glance link below:

Gross Output

Gross Output is a measure that may be more useful than the Gross Domestic Product (GDP) measure, as it looks at the top line of national income accounting. It is also a good measure to use in conjunction with GDP to get a better overall picture of the economy. This measure can be accessed by clicking the links below:

Surveys of Professional Forecasters

The Survey of Professional Forecasters’ web page offers the actual releases, documentation, mean and median forecasts of all the respondents in the Fed’s Survey of Professional Forecasters. Click the following link to be taken to the Federal Reserve Bank of Philadelphia’s website to access the current survey: Survey of Professional Forecasters.

The Livingston Survey of Professional Forecasters’ web page offers the actual releases, documentation, mean and median forecasts of all the respondents in the Fed’s Livingston Survey. Click the following link to be taken to the Federal Reserve Bank of Philadelphia’s website to access the current survey: Livingston Survey.

Econoday

Econoday offers some excellent resources for understanding and forecasting the economy. The link below takes you to Econoday’s Economic Calendar and Economic Events and Analysis sections. Please see Econoday’s Economic Calendar for upcoming economic reporting events in the week and months ahead.

AAII Investor Sentiment Survey

The AAII Investor Sentiment Survey measures the percentage of individual investors who are bullish, bearish, and neutral on the stock market for the next six months: AAII Investor Sentiment Survey.